Economic concerns should make you cautious, not scare you into panic.

Every investor over the last three months seems to have become a part-time economist. Discussions centre around anticipating Bernanke’s next big move, the future of the rupee, and how the RBI can be the new messiah pulling our economy out of the morass. Since these topics significantly impact our day-to-day lives in the form of high inflation, higher interest rates, and prospective income growth, it is no surprise that we see curiosity building in the public on these matters. It is time to come to terms with the volatility, learn to live with the risk, and even appreciate it.

We are in no position to predict the next move by the US Fed and the RBI, or, when inflation will come down or even where the rupee will go in the future. When the rupee touched 68, nobody dared to say that it would be back to 61 levels. Similarly, investment professionals have been repeatedly forecasting that inflation would be tamed in the next few months. Surprisingly, the goalpost keeps moving further and further. Even last week, it was a foregone conclusion that the US Fed would taper the monthly bond buying programme (quantitative easing) and that it was a “done deal”. But Bernanke thought otherwise. He delayed the taper, surprised everybody and brought about a big relief rally in the stock, currency and bond markets, leaving doomsayers high and dry.

NO PREDICTING

I am convinced there is no point getting into the prediction game. Rather, it is important to try and make some sense of the longer term patterns. The numbers show there is a definitive revival in the US. This means QE is on its way out. What we don’t know is when the exit will happen.

Our investment portfolios and strategies should be tuned keeping this in mind. Similarly, one cannot say when inflation would come under control or interest rates would fall. As investors, what we can do is that we can take advantage of this opportunity to lock-in higher yields by investing in fixed income products and in tax-free bonds. The yield on tax-free bonds is linked to the yield on the 10 year g-sec benchmark. Recent issuances of Tax-free bonds have carried attractive yields as 10-year G-sec yields remained high over the last three months. For most part of September this year, 10-year G-Sec yield has been in the range of 8.3 per cent to 8.5 per cent. Forthcoming issuances of tax-free bonds can thus carry yields up to 8.5 per cent, which is equivalent to a pre-tax yield of 12 per cent (on taxable instruments), and that too from government institutions.

A big roll-out of fixed maturity plans (FMPs) has been witnessed over the last couple of months. In the current scenario, almost all of these should carry yields in the range of 9.5 per cent to 11 per cent, with good credit quality. The net return to investors can, therefore, be very attractive. This is another mode of cashing in on the opportunities arising when interest rates are high.

Volatility is also the best friend of systematic investment plans in equity funds. SIPs help you accumulate more stocks during bad times thereby bringing your average cost down, and enable you to reap larger gains when the going is good. Concerns on economic and other headwinds should make you cautious, not scare you into inaction or panic. It is important that we continue our SIPs and, under no circumstances, panic and terminate them.

REASON TO SMILE

After a gloomy three-month period since May 2013, stock markets gave us a reason to smile in September. The entire fall that took place since May 22, 2013, the day the US Fed started the QE taper talk, was recovered in less than a month. Bluechip stocks are up anywhere between 25 per cent and 50 per cent from their August 2013 lows. Any mutual fund scheme having higher exposure to these stocks would have given better returns to investors.

Governor Raghuram Rajan has clearly stated he is serious about executing the RBI’s primary mandate of “monetary stability” which ultimately means low and stable inflation expectations. He also spoke of inclusive growth and financial stability. So, while everyone was expecting him to cut rates to revive growth, he hiked the repo rate to counter inflation expectations. But at the same time he cut the marginal standing facility rate and reduced the cash reserve ration daily maintenance requirements.

As investors, we should thus expect consistent efforts from the RBI going ahead, to bring inflation under control while taking care not to jeopardise growth and financial stability. This justifies higher allocations to fixed income, debt funds and tax-free bonds while maintaining equity allocations at a pre-decided level.

(The author is Vice-Chairman and MD, Bajaj Capital.)

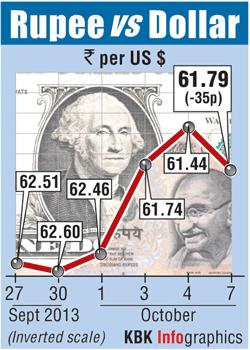

The rupee snapped a two-day winning streak on Monday, weighed down by weakness in domestic shares and hurt by broad-based dollar buying from importers and banks.

The rupee snapped a two-day winning streak on Monday, weighed down by weakness in domestic shares and hurt by broad-based dollar buying from importers and banks.